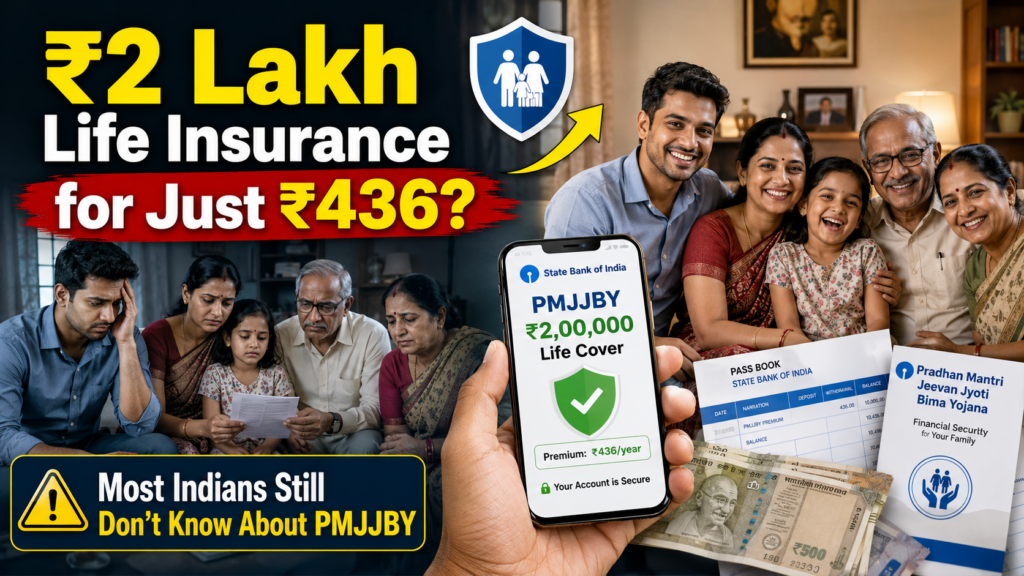

Life insurance is often ignored until a financial emergency hits a family. Many households in India still do not have affordable life cover. This is where Pradhan Mantri Jeevan Jyoti Bima Yojana, also known as PMJJBY, becomes important.

PMJJBY is a government-backed life insurance scheme designed for people who want low-cost financial protection. For an annual premium of just ₹436, you get life insurance coverage of ₹2 lakh. The scheme is especially useful for salaried employees, daily wage workers, small business owners, farmers, and people with limited income.

If you are looking for an affordable term insurance plan in India, PMJJBY can be one of the simplest ways to secure your family financially.

What is Pradhan Mantri Jeevan Jyoti Bima Yojana PMJJBY

PMJJBY is a one-year renewable life insurance scheme launched by the Government of India. The scheme is managed through banks and insurance providers.

The policy offers financial support to the nominee if the insured person dies due to any reason, including natural death or accident.

Key Highlights of PMJJBY

- Policy Coverage: ₹2 lakh life insurance cover

- Annual Premium: ₹436 per year

- Age Limit: 18 to 50 years for enrollment

- Coverage Period: 1 June to 31 May every year

- Type of Insurance: Pure term life insurance

- Claim Benefit: Paid to nominee after death of insured person

- Renewal: Auto-debit facility available

Why PMJJBY Matters for Indian Families

- Many families depend on one earning member. If that person dies unexpectedly, the family may struggle with rent, school fees, loans, and daily expenses.

- PMJJBY helps reduce this financial risk at a very low cost.

Example:

Ramesh, a delivery executive in Chennai, earns ₹18,000 per month. He enrolled in PMJJBY through his savings account. After his sudden death due to illness, his wife received ₹2 lakh under the scheme. The amount helped her pay rent and continue her daughter’s education during a difficult period.

This is why PMJJBY is considered one of the best low-cost government insurance schemes in India.

Objectives of PMJJBY

- Provide affordable life insurance to all citizens

- Increase financial inclusion in India

- Support low-income and middle-income families

- Encourage people to adopt insurance coverage

- Reduce financial stress after the death of an earning member

- Promote banking and digital financial services

Benefits of PMJJBY

- Affordable Premium: You pay only ₹436 per year. This makes PMJJBY one of the cheapest life insurance schemes in India.

- Life Cover of ₹2 Lakh: The nominee receives ₹2 lakh if the insured person dies during the policy period.

- Covers Natural and Accidental Death: Unlike some insurance plans that focus only on accidental death, PMJJBY covers death due to illness, accident, or natural causes.

- Easy Enrollment: You can apply through your bank account with minimal paperwork.

- Auto-Debit Facility: The annual premium gets automatically deducted from your bank account. This reduces the chance of policy lapse.

- Government-Supported Scheme: The scheme is backed by the Government of India, which increases trust among policyholders.

- Tax Benefits: Premium paid under PMJJBY may qualify for tax deductions under Section 80C of the Income Tax Act.

Who Should Buy PMJJBY

PMJJBY is suitable for:

- Daily wage workers

- Small shop owners

- Drivers and delivery workers

- Farmers

- Housewives with bank accounts

- Young salaried employees

- People without existing life insurance

- Senior earning members of low-income households

Even if you already have a private term insurance policy, PMJJBY can act as additional basic coverage.

Insurance Enrolment Period and Premium Details

The insurance scheme follows a yearly coverage cycle from 1 June to 31 May. Subscribers are encouraged to enroll before the beginning of the policy year to receive full coverage benefits.

The highlight of this scheme is its quarter-based premium structure. The premium amount reduces as the coverage period becomes shorter, making the plan affordable even for late enrolments. This flexible pricing model helps more people access financial protection throughout the year.

Premium Amount Based on Enrolment Period

| Enrolment Period | Quarter | Premium Amount |

|---|---|---|

| June, July & August | Q1 | ₹436 |

| September, October & November | Q2 | ₹342 |

| December, January & February | Q3 | ₹228 |

| March, April & May | Q4 | ₹114 |

Eligibility Criteria for PMJJBY

To join PMJJBY, you must meet these conditions:

- You must be an Indian citizen

- Age should be between 18 and 50 years

- You must have an active savings bank or post office account

- You should agree to auto-debit of premium

- You must provide consent for joining the scheme

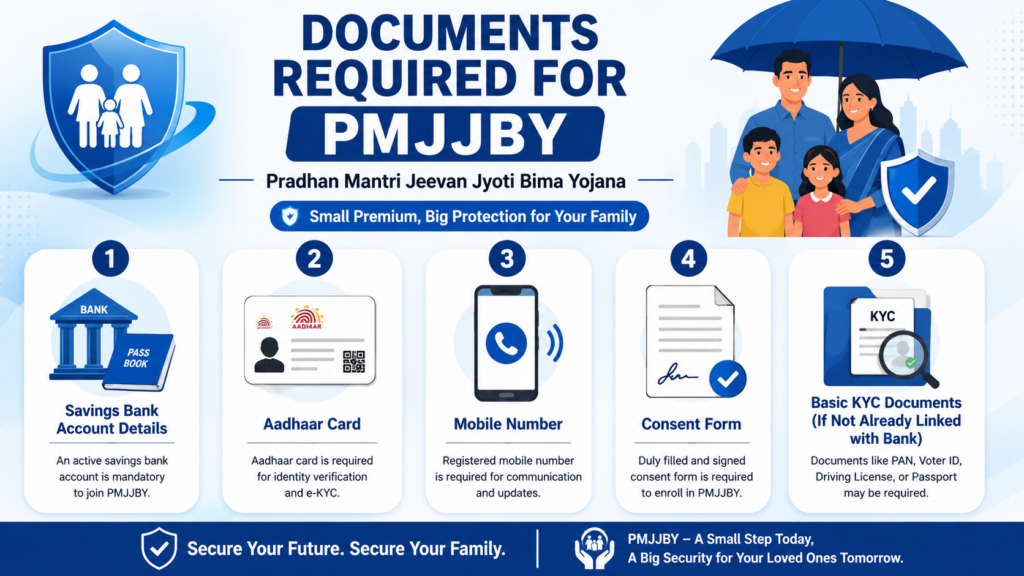

Documents Required for PMJJBY

- Savings bank account details

- Aadhaar card

- Mobile number

- Consent form

- Basic KYC documents if not already linked with bank

How to Apply for PMJJBY

Offline Process Through Bank

- Visit your bank branch

- Ask for the PMJJBY application form

- Fill in your details

- Submit Aadhaar and bank details

- Sign the auto-debit consent

- The bank activates your insurance coverage

Online Process

Many banks allow online enrollment through:

- Internet banking

- Mobile banking apps

- SMS banking

Example:

Several major banks like State Bank of India and Punjab National Bank allow eligible account holders to enroll digitally.

PMJJBY Claim Process

If the insured person dies, the nominee should:

- Inform the bank immediately

- Collect the claim form

- Submit death certificate

- Provide identity proof and bank details

- Submit canceled cheque or passbook copy

- After verification, the claim amount is transferred to the nominee’s bank account.

Download the Claim form of Post Office

Common Reasons Why PMJJBY Claims Get Delayed

- Incorrect nominee details

- Inactive bank account

- Insufficient balance during premium deduction

- Mismatch in Aadhaar and bank records

- Delay in submitting claim documents

- Unclear death certificate information

Common Mistakes to Avoid While Applying for PMJJBY

- Ignoring nominee updates after marriage

- Not maintaining minimum bank balance

- Providing incorrect mobile number

- Assuming enrollment is automatic

- Missing annual renewal checks

- Using dormant bank accounts

- Not informing family members about the policy

PMJJBY vs Regular Term Insurance

| Feature | PMJJBY | Private Term Insurance |

| Premium | Very low | Higher |

| Coverage Amount | ₹2 lakh | ₹25 lakh to ₹1 crore+ |

| Medical Test | Usually not required | Often required |

| Purpose | Basic financial support | Full financial protection |

| Best For | Low-income households | Long-term financial planning |

PMJJBY should not replace a full term insurance plan if you have dependents and higher financial responsibilities. It works best as a basic safety net.

PMJJBY and PMSBY Difference

People often confuse PMJJBY with Pradhan Mantri Suraksha Bima Yojana.

PMJJBY provides life insurance for death due to any reason.

PMSBY provides accidental insurance coverage only.

Many people enroll in both schemes because the combined annual premium is still very affordable.

Read more PMSBY – Pradhan Mantri Suraksha Bima Yojana

How PMJJBY Supports Financial Inclusion in India

According to government data, crores of Indians have enrolled in PMJJBY since launch. The scheme has helped expand insurance access in rural and semi-urban India where life insurance penetration was traditionally low.

For families living paycheck to paycheck, even a ₹2 lakh support amount can make a significant difference during emergencies.

Real-Life Use Cases of PMJJBY

Case 1

A farmer in Tamil Nadu enrolled through his rural bank branch. After his death due to a heart attack, the insurance amount helped his family repay agricultural loans.

Case 2

A security guard in Bengaluru enrolled through mobile banking. His nominee received claim support within weeks after an unexpected accident-related death.

Case 3

A factory worker combined PMJJBY with PMSBY. His family received support from both schemes after a fatal road accident.

Important Things You Should Know Before Enrolling

- The scheme renews every year

- Premium may change based on government decisions

- Only one PMJJBY policy is allowed per person

- Joint account holders can enroll separately

- Coverage ends if premium is not deducted

- You should keep nominee details updated regularly

PMJJBY is one of the most practical and affordable government insurance schemes available in India today. For less than the cost of a monthly mobile recharge, you can secure basic financial protection for your family.

If your family depends on your income, delaying life insurance is risky. PMJJBY offers a simple starting point for financial security, especially for first-time insurance buyers and low-income households.

Even though ₹2 lakh may not fully replace long-term income, it can provide immediate support during a financial crisis. That support can help your family manage expenses, repay loans, and maintain stability during difficult times.

Read more

PM Surya Ghar Muft Bijli Yojana, Get 300 Units Free Electricity at Home