Many Indian families still struggle with financial emergencies caused by accidents, medical issues, or the death of a family member. For people working in unorganized sectors, daily wage jobs, farming, small businesses, or gig work, one unexpected event can disturb the entire household income.

To address this challenge, the Government of India launched three social security schemes under the Jan Suraksha initiative:

- Pradhan Mantri Suraksha Bima Yojana (PMSBY)

- Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY)

- Atal Pension Yojana (APY)

These schemes were designed to offer low-cost insurance and pension coverage. The goal was simple. Make financial security accessible to every citizen, especially low-income and rural households.

As these schemes complete 11 years, their impact is visible across India through increased insurance coverage, pension awareness, and financial inclusion.

What Are Jan Suraksha Schemes?

Jan Suraksha schemes are government-backed social security programs aimed at protecting citizens from financial risks related to death, accidents, and old age.

The schemes focus on affordability and easy enrollment.

Overview of the Three Schemes

PMSBY

Provides accidental death and disability insurance. More than 27.43 crores have enrolled in which the female candidate alone are 12.72 crores.

PMJJBY

Offers life insurance coverage in case of the policyholder’s death. Over 58.09 crores people in which 27.45 crores are female have enrolled in the scheme

APY

Helps subscribers build a guaranteed pension after retirement. More than 9.04 crores have enrolled.

Why These Schemes Matter in India

India has a large workforce employed in the informal sector. Many workers do not receive employer-sponsored insurance or retirement benefits.

These schemes help bridge that gap by offering:

- Affordable premiums

- Easy access through banks

- Government-backed security

- Financial support during emergencies

- Retirement income for senior years

Example

A delivery worker earning ₹18,000 per month may not be able to afford expensive private insurance plans. But with PMSBY and PMJJBY, that worker can get both accident and life insurance coverage for a small yearly premium.

Similarly, a street vendor or domestic worker can join APY and build pension support for retirement.

PMSBY Explained

What is PMSBY?

Pradhan Mantri Suraksha Bima Yojana is an accident insurance scheme launched to provide financial support in case of accidental death or disability.

Current Premium: ₹20 per year

Coverage Benefits

- ₹2 lakh for accidental death

- ₹2 lakh for total disability

- ₹1 lakh for partial disability

Eligibility

- Age between 18 and 70 years

- Active savings bank account

- Consent for auto-debit

How PMSBY Helps Families

If a person dies in a road accident, the nominee receives ₹2 lakh. This amount can help the family handle immediate expenses, loans, children’s education, or household needs.

Real-Life Use Case

Imagine a construction worker traveling daily for work. One accident can stop the family’s income immediately. PMSBY provides financial relief at a very low cost.

To Know more about the scheme PMSBY

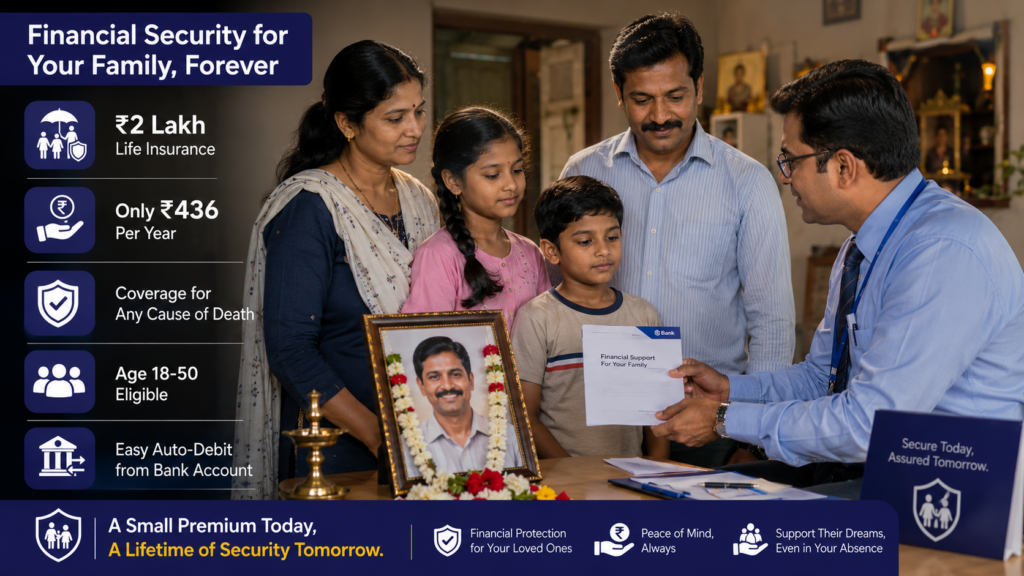

PMJJBY Explained

What is PMJJBY?

Pradhan Mantri Jeevan Jyoti Bima Yojana is a government-backed life insurance scheme.

Current Premium: ₹436 per year

Coverage Benefits: ₹2 lakh life insurance coverage in case of death due to any reason.

Eligibility

- Age between 18 and 50 years

- Savings bank account holder

- Auto-debit approval

Policy Duration: One-year renewable policy

Why PMJJBY Is Important

- Many families depend on a single earning member. If that person dies unexpectedly, the family often faces financial hardship.

- PMJJBY helps reduce this burden by offering life insurance at a low premium.

Example

A small shop owner with two school-going children enrolls in PMJJBY. If something unfortunate happens, the insurance payout can help the family manage education and household expenses during difficult times.

To Know more about the scheme PMJJBY

APY Explained

What is Atal Pension Yojana?

Atal Pension Yojana is a pension scheme focused mainly on workers in the unorganized sector.

Subscribers contribute regularly until retirement age and receive guaranteed monthly pension after the age of 60.

Pension Options: ₹1,000 to ₹5,000 monthly pension

Eligibility

- Age between 18 and 40 years

- Savings bank account

- Indian citizen

Key Benefits of APY

- Guaranteed pension after retirement

- Government-backed scheme

- Encourages long-term savings

- Provides financial independence in old age

Contribution Amount

Monthly contribution depends on:

- Entry age

- Desired pension amount

Younger subscribers contribute lower amounts.

Example

If a 25-year-old starts contributing early, the monthly payment remains affordable while ensuring pension support after retirement.

Benefits of Jan Suraksha Schemes

Affordable Financial Protection: These schemes are designed for ordinary citizens. Even low-income workers can afford the premiums.

Simple Enrollment Process

People can apply through:

- Banks

- Post offices

- Online banking platforms

Auto-Debit Convenience: Premiums are automatically deducted from bank accounts.

Encourages Financial Inclusion

The schemes motivate people to:

- Open bank accounts

- Use digital banking

- Participate in formal financial systems

Objectives of PMSBY, PMJJBY and APY

- Increase insurance penetration in India

- Provide social security to low-income citizens

- Promote pension awareness

- Reduce financial vulnerability

- Support financial inclusion initiatives

- Create long-term savings habits

Government Data and Growth

Over the last 11 years, these schemes have seen massive enrollment growth across urban and rural India.

Key achievements include:

- Crores of insurance enrollments

- Expansion through public and private banks

- Increased awareness about social security

- Higher participation from women and rural citizens

The schemes have become an important pillar of India’s financial inclusion strategy linked with Jan Dhan accounts and digital banking services.

Who Should Apply for These Schemes?

These schemes are especially useful for:

- Daily wage workers

- Farmers

- Delivery workers

- Drivers

- Domestic workers

- Shop owners

- Gig economy workers

- Self-employed individuals

- Young earners starting careers

Even salaried employees can benefit because of the low premium and additional financial protection.

Things You Should Know Before Enrolling

- Keep sufficient bank balance for premium deduction.

- Update nominee details regularly.

- Renew policies on time if required.

- Read policy conditions carefully.

- Choose pension amount wisely in APY.

Common Mistakes to Avoid

- Ignoring nominee updates

- Maintaining low bank balance during auto-debit

- Assuming all bank accounts are automatically covered

- Missing renewal notifications

For many households, these programs provide a financial safety net during emergencies and old age. As awareness grows, more citizens are expected to participate in India’s social security ecosystem.

If you have not enrolled yet, these schemes can be a practical step toward protecting your family and planning your financial future.

Read more